Understanding the changing landscape of sustainability assurance in Canada

The September 2021 Audit Quality Blog introduced the topic of sustainability reporting and assurance and highlighted ongoing developments relevant to the profession. Since September, the demand for high-quality sustainability information has continued and there have been important announcements which demonstrate the crucial role the assurance profession will need to play to enhance the credibility of sustainability information.

In this blog, we will cover:

- the recent developments and how they impact the assurance profession

- the current sustainability assurance landscape in Canada

- how these developments will impact the assurance profession

What are the recent developments and how do they impact the assurance profession?

Announcement of an International Sustainability Standards Board (ISSB) by the IFRS Foundation

In November 2021, the IFRS Foundation announced the formation of a new International Sustainability Standards Board (ISSB) to develop a comprehensive set of high-quality sustainability disclosure standards to meet the needs of investors. The establishment of the ISSB is a response to the growing demand to improve global consistency and comparability of sustainability reporting.

The ISSB will have a global and multi-location presence. Offices in Frankfurt, Germany (the seat of the board and the office of the chair) and in Montreal, Canada will be responsible for key functions supporting the new board and deeper co-operation with regional stakeholders. Offices in San Francisco, U.S. and London, U.K. will provide technical support to the new board.

CPA Canada is among the broad group of private and public institutions and organizations known as Canadian Champions for Global Sustainability Standards who backed the country’s offer to host the ISSB.

In November 2021, the IFRS Foundation also released two prototypes prepared by their Technical Readiness Working Group (TRWG) which will provide the basis for the ISSB to consider in preparing its first exposure draft of proposed standards:

- climate-related disclosure prototype - sets out the requirements for the identification, measurement and disclosure of climate-related financial information

- general requirements for disclosure of sustainability-related financial information prototype - sets out the requirements for disclosing sustainability-related financial information relevant to significant sustainability-related risks and opportunities

The Foundation also announced the consolidation of two voluntary sustainability standard-setters, the Value Reporting Foundation and the Climate Disclosure Standards Board, into the IFRS Foundation to provide technical expertise.

The ISSB will sit alongside and work closely with the International Accounting Standards Board (IASB) to ensure connectivity between the ISSB sustainability standards and IFRS accounting standards.

Canadian Securities Administrator (CSA) Proposed National Instrument 51-107 Disclosure of Climate-Related Matters

In October 2021, the CSA published a consultation for a proposed national instrument on the disclosure of climate-related matters by public Canadian issuers, other than investment funds; issuers of asset-backed securities; designated foreign issuers; SEC foreign issuers; certain exchangeable security issuers; and certain credit support issuers. Final responses to the consultation were received on February 16, 2022 and are currently being reviewed by the CSA.

Under the proposed instrument, companies would be required to disclose climate-related information under the four core elements of the Task Force on Climate Related Disclosures (TCFD) recommendations:

- governance - the organization's governance around climate-related risks and opportunities

- strategy - the actual and potential impacts of climate-related risks and opportunities on the organization's business, strategy and financial planning

- risk management - the processes used by the organization to identify, assess and manage climate-related risks

- metrics and targets - the metrics and targets used to assess and manage relevant climate-related risks and opportunities

The consultation included a question asking whether there should be a requirement for some form of assurance on greenhouse gas (GHG) emissions reporting.

As a result of the increased focus by regulators, companies could look to their assurance providers for input on the impact of these requirements to their reporting process and may consider the possibility of assurance over this information.

Independent Review Committee on Standard Setting in Canada

In 2021, the Independent Review Committee on Standard Setting in Canada (IRCSS) was established to conduct a review of the current governance and structure for establishing Canadian accounting and assurance standards, as well as what might be needed in the future – including sustainability standards. Its goal is to identify recommendations to ensure Canadian standards setting is independent, world-class and responsive to stakeholders’ needs.

It released a consultation paper to seek views and ideas on what should be done to best achieve this.

In the consultation, the IRCSS considers establishing a Canadian sustainability standards board that would work alongside Canada’s existing accounting and assurance standard-setting boards and liaise with the new international board.

Responses to the consultation are due March 31, 2022 and final recommendations from the IRCSS are planned for later in 2022.

The International Auditing and Assurance Standards Board (IAASB) responds to the demand for sustainability reporting

In the past, the IAASB has devoted significant energy to creating standards to govern assurance of non-financial information. They have a well-established umbrella standard, International Standard on Assurance Engagements (ISAE) 3000 Revised, Assurance Engagements Other than Audits or Reviews of Historical Financial Information and subject-matter specific standards such as At a Glance: International Standard on Assurance Engagements (ISAE) 3410, Assurance Engagements on Greenhouse Gas Statements.

In April 2021, the IAASB published guidance aimed at helping assurance professionals apply their umbrella standard to sustainability and other non-financial (or extended external reporting) assurance engagements.

They recognize the existing standards and guidance is only the beginning, a solid foundation to build upon. In early 2022, the IAASB approved their workplan for 2022-2023 and in it they agreed to dedicate capacity and resources to the assurance of sustainability or ESG reporting. Information gathering and research activities to determine future IAASB action started in January 2022. This initial work will also determine the precise scope and timing of the IAASB’s efforts.

The IAASB has indicated that their initial consultation could lead to:

- developing new subject matter-specific standard(s) that build on and supplement ISAE 3000 (Revised)

- targeted enhancements to ISAE 3000 (Revised), as necessary

- other related actions that are necessary in the public interest, for example, revising their existing guidance or developing new guidance

The Auditing and Assurance Standards Board (AASB) issues guidance on sustainability and other extended external reporting assurance in Canada

The AASB adopted the ISAE 3000 standard for use in Canada as CSAE 3000, Attestation Engagements Other than Audits or Reviews of Historical Financial Information and ISAE 3410 as CSAE 3410, Assurance Engagements on Greenhouse Gas Statements. There are some Canadian amendments to these standards, including the development of CSAE 3001, a separate standard for direct engagements. The September 2021 Audit Quality Blog introduced the Non-authoritative Guidance on Applying CASE 3000 to Sustainability and Other Extended External Reporting Assurance Engagements which practitioners can use for real-world assistance in applying CSAE 3000.

The AASB recognizes that the demand for assurance engagements that enhance stakeholder confidence in sustainability information is growing and committed in its 2022-2025 strategic plan to set high-quality standards and guidance that respond to the evolving needs and expectations of stakeholders. The AASB will also continue to monitor and provide input into the IAASB’s work.

The AASB continues to monitor other developments relating to the provision of assurance services regarding sustainability reporting and will undertake actions to proactively address evolving demand for these services as highlighted in the IRCSS consultation paper.

The International Federation of Accountants’ (IFAC) Vision for High-Quality Assurance of Sustainability Information

In December 2021, IFAC released their vision for sustainability assurance which addresses the importance of global standards, regulation that supports decision-useful disclosure, and the value of an interconnected approach to sustainability and financial information reporting and assurance. As stated within, "In order to be trusted, sustainability disclosure must be subject to high-quality, independent, external assurance. Best practices are emerging – founded on high-quality standards.”

What is the current sustainability assurance landscape in Canada?

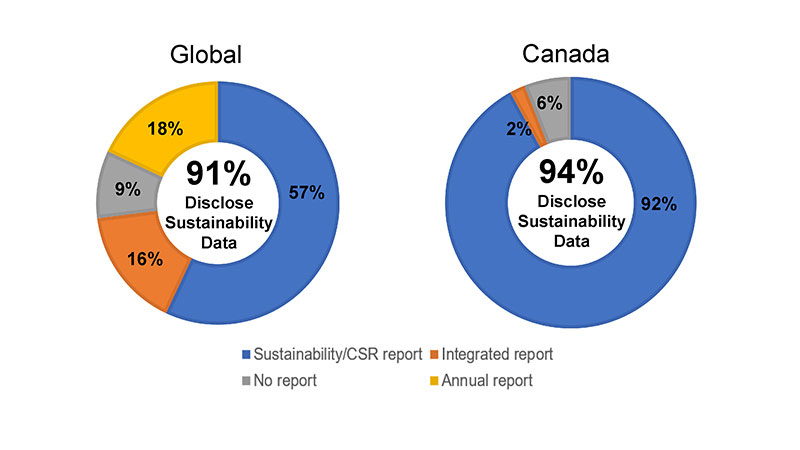

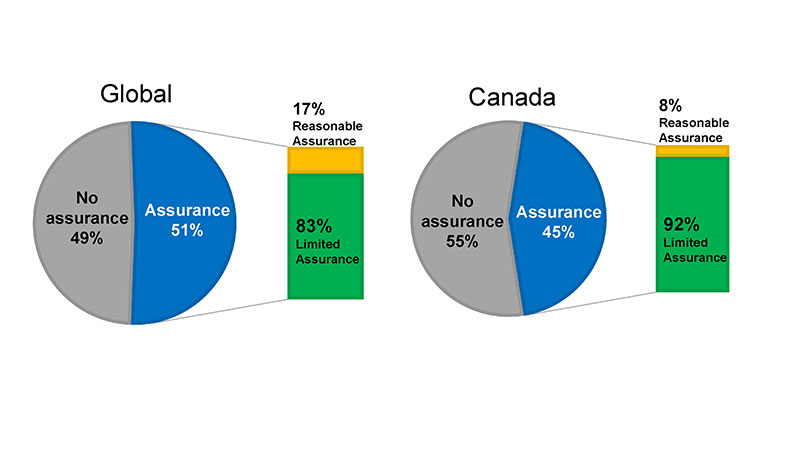

Before considering how these developments could impact the assurance profession in the future, it is important to understand the current sustainability assurance landscape. The September 2021 Audit Quality Blog introduced some key findings from The State of Play of Sustainability Assurance global benchmarking study, released by IFAC and the American Institute of CPAs (AICPA) and the Chartered Institute of Management Accountants (CIMA).

The report covers trends of the largest public companies and found that globally and in Canada, a majority of these companies reported some form of sustainability information.

Of these companies, some obtain some level of assurance over the sustainability information.

CPA Canada is conducting research to further explore sustainability assurance trends in Canada and investor expectations in this space which will explore the following:

- What level of assurance do investors need?

- Are they satisfied with the limited assurance they are currently receiving?

- Are the existing assurance frameworks appropriate to support investor needs?

- Who is permitted to perform assurance engagements and what qualifications are needed?

- What are the costs and benefits?

This research will include outreach with investors and assurance practitioners providing assurance over sustainability information.

How will these developments impact the assurance profession?

Increased interest from investors, changes to regulation and the movement towards a global set of sustainability standards will lead more companies to report on their sustainability information. Organizations will look to CPAs to provide guidance on how to incorporate sustainability into their business strategy and their reporting structures.

As the sustainability landscape continues to evolve, it is crucial for assurance providers to remain cognizant of the impacts to their clients’ changing business activities and to respond to their assurance needs. Performing these services will require practitioners to invest in additional training and education.

To help practitioners learn more about sustainability, CPA Canada has developed a variety of resources highlighted on our sustainability assurance resources hub. We have also created a resource page for finding the right service or engagement that will best meet your client’s needs.

Want to be involved in future CPA Canada research on sustainability assurance?

Are you currently involved in providing assurance over sustainability information? Are you interested in being involved in the future work that CPA Canada undertakes related to sustainability assurance? Please email us directly about opportunities to participate in this important research.

Keep the conversation going

Do you have additional questions on how to support your clients' current and future sustainability assurance needs? What are your views regarding the CPA profession's role in sustainability assurance? Please post a comment below or email us directly.

Disclaimer

The views and opinions expressed in this article are those of the author and do not necessarily reflect that of CPA Canada.