Navigating the CPA Canada Roadmap Tool: Assurance standards for your engagements

Our roadmap tool can help practitioners identify which standard(s) to use when providing services in accordance with the CPA Canada Handbook — Assurance. This page provides helpful information for using the tool.

Have you received requests for assurance services and weren't sure which assurance standard was appropriate? Did you know that some third-party requests may include two subject matters and therefore you may need to undertake two separate engagements and issue two opinions? To help identify which standard(s) to use and when, we've developed the CPA Canada Roadmap Tool to assist you when providing services in accordance with the CPA Canada Handbook — Assurance.

This blog is for practitioners providing services in accordance with the Handbook. Continue reading to learn:

- what is the tool

- why it was created

- how you can use it effectively

- who will benefit from it

What is the Roadmap Tool?

The tool is an interactive application designed to ask a series of branching questions to help you navigate the Handbook. The tool walks you through a series of questions related to the request and then provides a recommended conclusion regarding the primary standard to use in light of the facts and circumstances of the request.

Keep in mind, the tool does not replace the need to read the entire applicable standard(s), including the application and other explanatory material, and it is not appropriate to rely on the tool's conclusion(s) as audit evidence. Please ensure that you have the proper accounting licence to perform the engagements recommended by the tool, and check with your provincial institute and ensure you follow the applicable rules of professional conduct.

Why did CPA Canada create the Roadmap Tool?

The Handbook contains various standards to assist you as an assurance practitioner in performing many different types of engagements with varying levels of assurance provided. It can sometimes be difficult, based on the nature of the request, to determine which standard(s) to report in accordance with. Often, the confusion arises because the request is unclear. Third parties are typically unfamiliar with the standards in the Handbook and the terminology used by assurance practitioners.

This knowledge gap often leads to vague or outdated requests, where the third party is often asking the practitioner to report in accordance with an assurance standard that is no longer effective. All these factors require the practitioner to exercise their professional judgment to interpret the nature of the request.

Moreover, there are many situations when a third party may issue one request that includes two subject matters and two different reporting needs, requiring a practitioner to report in accordance with two different standards to meet the needs of the intended user. If the practitioner does not identify the need to report in accordance with two different standards (i.e., therefore undertaking two separate engagements) it could lead to incomplete planning and execution of audit procedures and the inappropriate issuance of a practitioner's deliverable. When there are multiple subject matters in one request, it may sometimes be referred to as a "multi-scope" engagement. Often these "multi-scope" engagements create confusion regarding which assurance standards are appropriate and as such the tool allows you to select more than one subject matter, so that all applicable standards to report in accordance with can be identified. Examples of subject matter included in the tool are:

- annual financial statements

- controls at a service organization

- historical financial information other than financial statements

- internal control over financial reporting

- compliance with agreements and regulations

- future-oriented financial information (financial forecasts or projections)

Example request

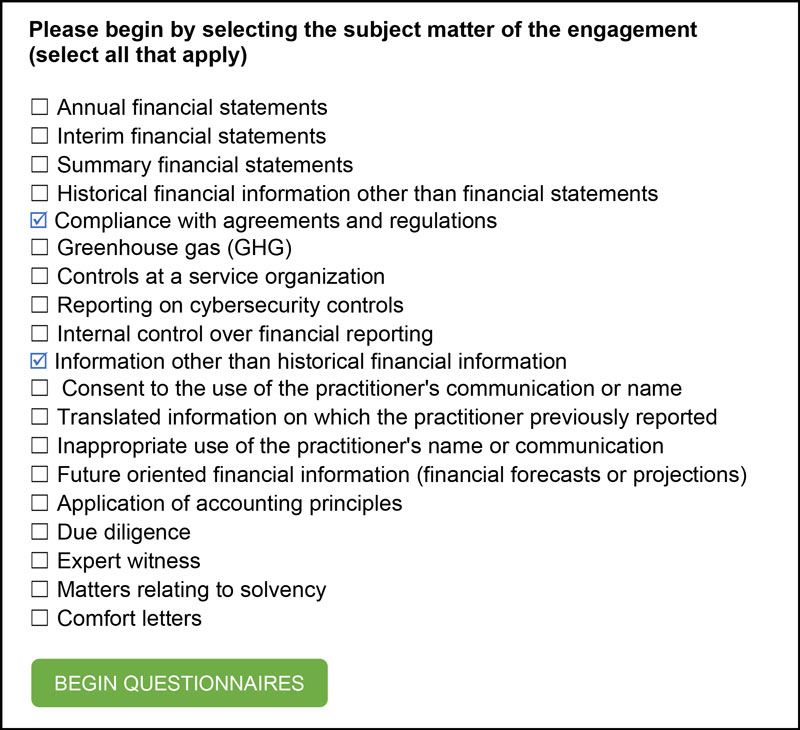

You have received one request from a private career college (PCC). The PCC has been requested by the Ontario Ministry of Colleges and Universities to engage a practitioner to provide:

- an opinion on the enrollment and graduate data against the ministry's criteria

- an opinion on the enrollment and graduate data that provides assurance that the information in the file has not been misstated

Specifically, you have been asked to compare graduation status and graduate record of sampled students recorded in the graduate data files to the official student record that is used to generate transcripts.

In this example, it appears the third party is requesting two different engagements with two different subject matters:

- compliance with agreements and regulations (i.e., in accordance with Canadian Standard on Assurance Engagements (CSAE) 3530, Attestation Engagements to Report on Compliance or CSAE 3531, Direct Engagements to Report on Compliance)

- information other than historical financial information (i.e., in accordance with CSAE 3000, Attestation Engagements Other than Audits or Reviews of Historical Financial Statements or CSAE 3001, Direct Engagements)

In this case, you would select both subject matters in the tool (see image below) and proceed to answer the relevant questions about both subject matters. The tool would then provide you with a recommendation on each subject matter for your consideration. Note the request may not always be clear on what the subject matters are or that two opinions are requested.

How do I use the Roadmap Tool?

The tool is an easy-to-use online application which allows you to select a variety of subject matters and then walks you through questions to see if the request falls under the Handbook standards. Before you can begin, it is helpful to understand who the request is coming from and who you will be reporting to. It is also important to understand the scope and nature of work you will need to perform, as well as the level of assurance the requesting party is seeking. If the request is not clear, or if there are undefined terms within the request (e.g. certify, approve, sign off, etc.) then you may need to clarify the request with the requesting party or have your client clarify the request with the requesting party.

CPA Canada has prepared a Guide for Practitioners: Roadmap to the CPA Canada Handbook — Assurance Tool to help you select the appropriate subject matter related to the request. To assist you in understanding the subject matter options used in the tool, the guide includes background information on the different subject matters as well as example engagements.

Who can benefit from the Roadmap Tool?

Practitioners providing service in accordance with the Handbook will find the Tool useful and user-friendly. Given the recent updates and changes to the Handbook, a practitioner may be unsure which standard is relevant for their engagement. For example, in recent years, the following standards have been issued or effective:

- CSAE 3530, Attestation Engagements to Report on Compliance / CSAE 3531, Direct Engagements to Report on Compliance (effective for compliance reports dated on or after April 1, 2019) replaced:

- Section 5800, Special Reports — Introduction

- Section 5815, Special Reports — Auditor's Reports on Compliance with Agreements, Statutes and Regulations

- Section 8600, Reviews of Compliance with Agreements and Regulations

- Paragraphs .11-.13 of PS Section 5300, Auditing for Compliance with Legislative and Related Authorities in the Public Sector

CSRS 4400, Agreed-upon Procedures (AUP) Engagements (effective for AUP engagements for which the terms of engagement are agreed on or after January 1, 2022) replaces:

- Section 9100, Reports on the Results of Applying Specified Auditing Procedures to Financial Information Other than Financial Statements

- Section 9110, Agreed-upon Procedures Regarding Internal Control over Financial Reporting

Therefore, it can be helpful to use the tool to check whether you have considered the most recently issued standard(s) as you determine engagement acceptance. In most cases, the tool will also recommend and link you to any available non-authoritative guidance and link you directly to the Handbook section.

Get additional resources on auditing and assurance standards

We are committed to supporting Canadian practitioners and members in industry to better understand and apply auditing and assurance standards, including Canadian Auditing Standards (CAS) and other assurance standards. With this objective in mind, we offer a variety of high-quality guidance and support resources.

The Audit and Assurance Resource Guide provides a summary of our audit and assurance resources, including:

- audit and assurance alerts

- client briefings

- implementation tools

- guides

- webinars

Keep the conversation going

Have you had a chance to check out the CPA Canada Roadmap Tool? Was it helpful in walking you through the CPA Canada Handbook — Assurance? Were there questions that arose as you used the tool? Do you have suggestions on how to improve the tool? We are very interested in hearing your questions and comments on the tool as we look to continuously improve its functionality. Post a comment below or email us directly.

Conversations about Audit Quality is designed to create an exchange of ideas on global audit quality developments and issues, and their impact in Canada.

Disclaimer

The views and opinions expressed in this article are those of the author and do not necessarily reflect that of CPA Canada.