PSAB: Reviewing our approach to International Public Sector Accounting Standards (IPSAS)

The Public Sector Accounting Board (PSAB) released its first consultation paper on the International Strategy project in May 2018. This initial consultation paper introduced stakeholders to the decision-making criteria PSAB will consider when evaluating the international strategy.

The purpose of Consultation Paper 2, Reviewing PSAB’s Approach to International Public Sector Accounting Standards is to:

- summarize respondents’ feedback on the initial 2018 consultation paper, notably the decision-making criteria and options outlined

- clarify the options

- describe the updated decision-making criteria that reflects the feedback

- apply the updated criteria to each of the options

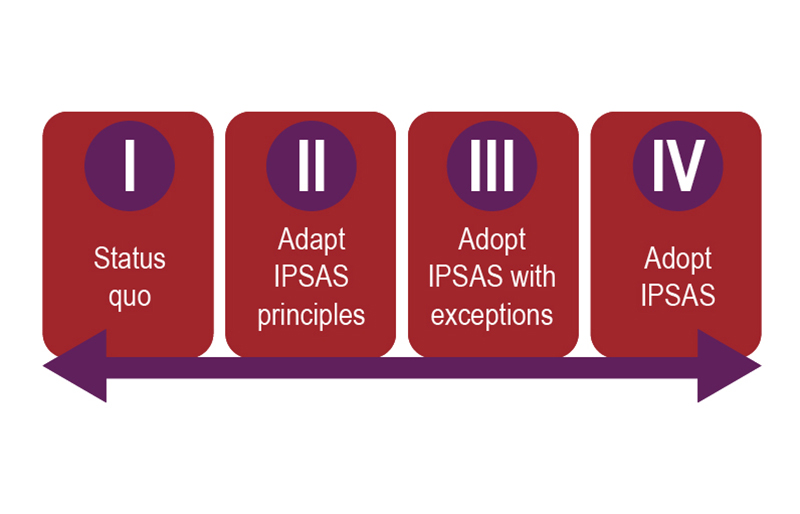

Based on the feedback provided to the first consultation paper, PSAB refined the four options.

- Status quo: Continue with the existing Canadian standard-setting process, with PSAB independently establishing Public Sector Accounting Standards (PSAS).

- Adapt IPSAS principles: Continue to develop PSAS, but future standards would be based on the principles in each existing IPSAS as it is considered for Canadian adoption. If a project is undertaken and an IPSAS already exists, the principles of that standard would be used as a base for developing the PSAS.

- Adopt IPSAS with exceptions: Adopts IPSAS as issued by the International Public Sector Accounting Standards Board (IPSASB), other than where a departure is deemed necessary to address Canadian circumstances.

- Adopt IPSAS: Adopt IPSAS as issued by the IPSASB. Retrospective adoption of all IPSAS would occur at a defined transition date. PSAB would maintain a strong global presence on the international stage to enhance Canada’s influence.

Responses to this second consultation paper are due by September 30, 2019.

PSAB will deliberate on the feedback and expects to be able to decide on its approach to IPSAS at its March 2020 board meeting. Key in the decision-making process is understanding stakeholders’ viewpoints.

Contact

Thaksa Sethukavalan, principal, Public Sector Accounting Board