An Introduction to IFRS Sustainability Disclosure Standards

What is the International Sustainability Standards Board (ISSB) and why is it important for Canadian stakeholders to respond to the ISSB’s consultation?

International investors and a range of other stakeholders are increasingly calling on companies to disclose high-quality information on their sustainability performance that is transparent, reliable and comparable.

Historically, companies have used a variety of frameworks and standards from voluntary organizations to disclose sustainability information which has resulted in concerns about the reliability, usefulness, and comparability of such information.

Recent global and Canadian developments, including the development of an International Sustainability Standards Board (ISSB) by the International Financial Reporting Standards (IFRS) Foundation, intend to enhance the disclosure of sustainability information and create global convergence through the development of IFRS Sustainability Disclosure Standards.

What is the IFRS Foundation’s Sustainability Project and the International Sustainability Standards Board (ISSB)?

In 2020, the IFRS Foundation issued a formal consultation paper, which addressed sustainability reporting and whether there is a need for global sustainability standards. Response to the consultation confirmed the growing and urgent demand for global sustainability reporting standards and support for the IFRS Foundation to play a role in their development.

At the UN Climate Change Conference (COP26) in November 2021, the IFRS Foundation Trustees announced the creation of the ISSB, a new standard-setting board within the IFRS Foundation. The ISSB’s remit is to issue standards that deliver a comprehensive global baseline of sustainability-related financial disclosures for the capital markets.

The new board will operate alongside the International Accounting Standards Board (IASB).

Source: IFRS Foundation

The ISSB will feature a global and multi-office structure. Centres in Frankfurt (the seat of the board and the office of the chair) and Montreal will be responsible for key functions supporting the new board and deeper co-operation with regional stakeholders.

IFRS Sustainability Disclosure Standards Exposure Drafts

In March 2022, the ISSB released two exposure drafts for public comment due July 29, 2022:

- IFRS S1 - General Requirements for Disclosure of Sustainability-related Financial Information

- IFRS S2 - Climate-related Disclosures

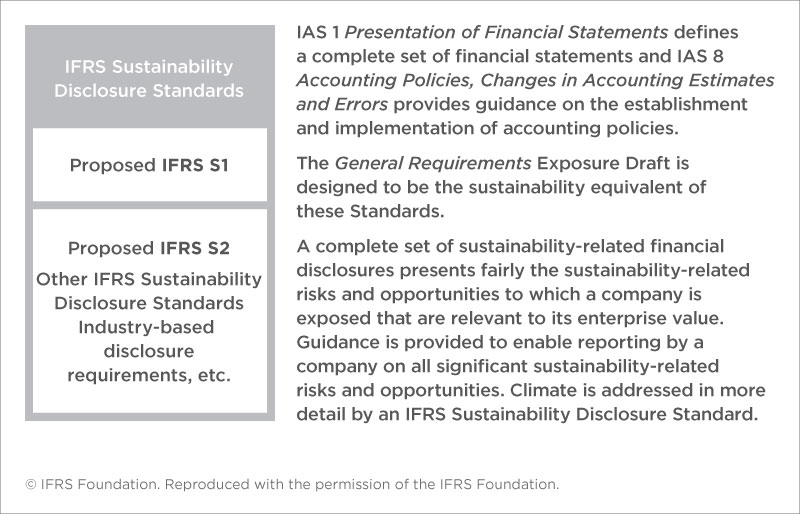

General Requirements Exposure Draft

To comply, a company would disclose material information about all significant sustainability-related risks and opportunities to which it is exposed. This information would need to be disclosed as a part of the company’s general purpose financial reporting.

The sustainability information disclosed would be centered on a company’s consideration of its governance, strategy, and risk management, as well as the metrics and targets it uses to measure, monitor and manage significant sustainability-related risks and opportunities.

Source: IFRS Foundation

Climate Exposure Draft

A company applying the proposals in the General Requirements Exposure Draft would apply the Climate-related Disclosures Exposure Draft to provide material information about its significant climate-related risks and opportunities.

To comply, a company would disclose information that would enable an investor to assess the effect of climate-related risks and opportunities on the company. It would require a company to centre its disclosures on the consideration of the governance, strategy and risk management of its business, and the metrics and targets it uses to measure, monitor and manage its significant climate-related risks and opportunities.

The proposed standard incorporates and builds on the recommendations of the Task Force on Climate related Financial Disclosures (TCFD) and includes industry-based disclosure requirements based on SASB Standards. A company would identify the requirements applicable to its business model and associated activities.

Why should Canadian stakeholders provide feedback on the exposure drafts?

The creation of the ISSB has been met with overwhelming support from Canadian companies. Montreal's selection as an ISSB centre is the result of a successful bid supported by large pension funds, financial institutions, securities regulators, a leading First Nations organization, accounting firms, insurance companies, and other large Canadian companies, along with the support of the country’s six largest municipalities and a broad cross-sector of Canada’s leading business, academic, and environmental stakeholder organizations. In April 2022, CPA Canada and the IFRS Foundation signed a memorandum of understanding (MOU) to establish the ISSB centre in Montreal.

Canadian regulators are monitoring ISSB developments that could influence their future regulations. Specifically, the Canadian Securities Administrators (CSA) published a consultation for a proposed national instrument on the disclosure of climate-related matters by public Canadian issuers, other than investment funds, issuers of asset-backed securities, designated foreign issuers, SEC foreign issuers, certain exchangeable security issuers, and certain credit support issuers. The CSA strongly supports the establishment of the International Sustainability Standards Board.

The Independent Review Committee on Standard Setting (IRCSS) is reviewing the governance structure for existing Canadian accounting, auditing, and assurance standards, as well as what might be needed for the future - including sustainability standards. The IRCSS is considering establishing a Canadian Sustainability Standards Board that would work alongside Canada’s existing accounting, auditing, and assurance standards bodies.

Your input on the ISSB Exposure Drafts is important. Provide your feedback for the General Sustainability-related Disclosures and Climate-related Disclosures by July 29, 2022.

Frequently asked questions

The frequently asked questions below and additional questions can be accessed in the IFRS Foundation’s Exposure Draft Snapshot.

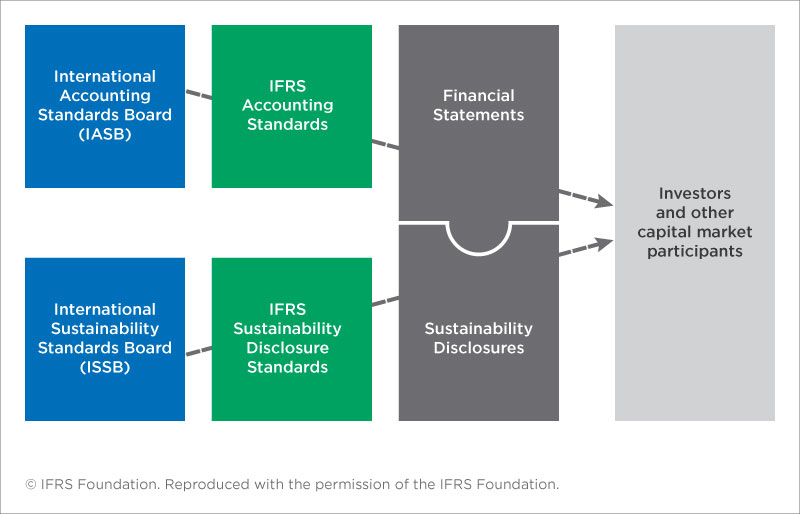

Would a company that applies IFRS Accounting Standards also be required to comply with IFRS Sustainability Disclosure Standards?

No, IFRS Accounting Standards apply to the financial statements. Even if a jurisdiction requires the application of IFRS Accounting Standards, it will decide whether companies under its jurisdiction will be required to comply with IFRS Sustainability Disclosure Standards.

The proposed General Requirements Exposure Draft would require a company to make a separate statement that it has complied with all the relevant requirements of IFRS Sustainability Disclosure Standards.

Would IFRS Sustainability Disclosure Standards be mandatory?

Jurisdictional authorities would decide whether to require the application of IFRS Sustainability Disclosure Standards, just as they have decided whether to require the application of IFRS Accounting Standards. The ISSB does not have the right to mandate the application of its standards. However, companies can choose to apply them. The Canadian Securities Administrators determine reporting requirements for Canadian public companies.

When are the proposed standards likely to come into effect?

One of the questions in the proposals is how long companies think they would need to prepare to apply the proposals.

The ISSB will consider all feedback on the proposals in compliance with the IFRS Foundation’s rigorous due process requirements and aim to finalize two IFRS Sustainability Disclosure Standards by the end of 2022. During these deliberations, the ISSB will consider the effective dates of the standards. Once the standards are issued, the requirements would be available for immediate voluntary adoption.

Does the ISSB have plans to develop additional IFRS Sustainability Disclosure Standards?

Later this year, the ISSB will consult on its standard-setting priorities. This consultation will include seeking feedback on other sustainability-related risks and opportunities relevant to the assessment of enterprise value and on further development of industry-based requirements, building on SASB standards.