Preparing for the new quality management standards

The new and revised quality management standards require all firms to design, implement and operate a system of quality management that applies to audits, reviews, as well as other assurance and related services engagements.

This blog provides:

- information on the standards, including their effective dates

- an update on conforming amendments to Other Canadian Standards

- tips and resources to prepare for implementation

The quality management standards

The Auditing and Assurance Standards Board (AASB) approved the new and revised quality management standards in January 2021. They include:

- Canadian Standard on Quality Management (CSQM) 1, Quality Management for Firms that Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements

- CSQM 2, Engagement Quality Reviews

- Canadian Auditing Standard (CAS) 220, Quality Management for an Audit of Financial Statements

- conforming amendments to other CAS

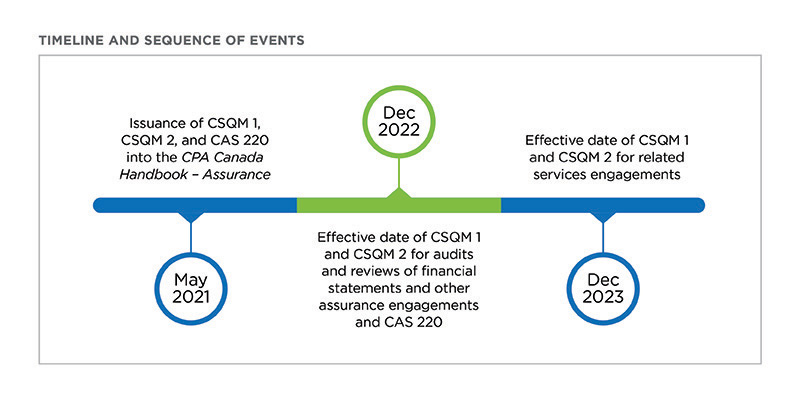

The standards were issued in the CPA Canada Handbook – Assurance in May 2021.

CSQM 1 requires firms to design, implement and operate a system of quality management. CSQM 1 takes a risk-based approach to quality management, which is a significant change from the previous standard. In addition, the AASB expanded the scope of the standard: the previous standard, Canadian Standard on Quality Control (CSQC) 1, Quality Control for Firms that Perform Audits and Reviews of Financial Statements, and Other Assurance Engagements, did not apply to related services engagements. CSQM 1 applies to all engagements for which there are standards in the CPA Canada Handbook – Assurance.

The AASB recognized that designing and implementing a system of quality management for the first time will be a significant undertaking. As a result, the AASB deferred the effective date of CSQM 1 as it applies to related services engagements by one year to December 15, 2023. Firms that perform other services, including audits, reviews and other assurance engagements, will need to have a system of quality management in place by December 15, 2022. The effective dates of the standards are explained in further detail below.

Conforming amendments to other Canadian standards

To complete the quality management project, including ensuring that quality management at the engagement-level is addressed in all standards, the AASB approved conforming amendments to Other Canadian Standards (OCS) in March 2022. The conforming amendments were published in the Handbook in May 2022.

The conforming amendments include revisions to all standards in the Handbook, other than CSQMs and CAS 220, to establish that CSQM 1 and CSQM 2 apply and to set out the engagement partner’s responsibilities for quality management at the engagement level. The effective dates of the conforming amendments vary depending on the nature of the engagement, as explained below.

When are the standards effective?

CSQM 1 requires firms to have their system of quality management in place for audits or reviews of financial statements, or other assurance engagements designed and implemented, by December 15, 2022. Recognizing the additional effort that may be required by firms designing and implementing a system of quality management for the first time, the AASB deferred the effective date for related services engagements by one year to December 15, 2023.

CSQM 2 is effective for audits and reviews of financial statements for periods beginning on or after December 15, 2022, for other assurance engagements beginning on or after December 15, 2022, and for related services engagements beginning on or after December 15, 2023.

CAS 220 is effective for audits of financial statements for periods beginning on or after December 15, 2022.

The effective dates of the engagement-level quality management conforming amendment requirements vary depending on the nature of the engagement, as follows:

- Review and other assurance engagement standards - The conforming amendments will generally be effective for engagements or periods beginning on or after December 15, 2022.

- Related services engagements that are performed in conjunction with, or following, an audit, review or other assurance engagement - The conforming amendments will be effective for engagements or periods beginning on or after December 15, 2022.

- Other related services engagements, including compilation engagements and agreed-upon procedures engagements - Practitioners have an extra year to align with the effective date of CSQM 1. For these engagements, the conforming amendments will be effective for engagements or periods beginning on or after December 15, 2023.

Every standard includes an explanation of the effective date. For more details on the effective dates, refer to the standards in the CPA Canada Handbook – Assurance.

Getting ready for implementation

How do I prepare and what resources are available?

The new and revised quality management standards are quite lengthy and detailed. Designing a system of quality management will involve considerable time and effort. You will need to consider the nature and circumstances of your firm and the engagements you perform, and design a system of quality management accordingly that is tailored to your firm. The first step will be to familiarize yourself with the standards by reading CSQM 1 and CSQM 2.

Implementation Tool

The International Auditing and Assurance Standards Board (IAASB) has prepared first-time implementation guides to assist practitioners in applying the new and revised standards. As CSQM 1 and CSQM 2 are adopted from the equivalent IAASB standards, you may wish to refer to the IAASB guides. The IAASB also produced several short videos that explain certain aspects of the standards. These various resources can be accessed here.

In addition, CPA Canada developed the Implementation Tool for Practitioners – A Focus on Firms that Perform Related Service Engagements. This tool is directed at firms that do not perform assurance engagements and will be designing and implementing a system of quality management for the first time. It includes a core document (36 pages) and individual appendices, which explore the various components more extensively. Examples and frequently asked questions relevant to smaller firms are included throughout. They consider the circumstances of firms that perform primarily non-assurance engagements, such as compilation engagements or agreed-upon procedures engagements.

Practitioner’s Pulse Webinars

In June 2021, CPA Canada hosted a webinar that highlighted the new and revised standards, including considerations for smaller firms as you prepare for implementation. You can access an on-demand recording of this event.

CPA Canada plans to host a webinar in June 2022, including a live discussion with practitioners who will share their experiences to date in developing quality management systems and applying the requirements of the new and revised quality management standards.

Other resources

You can find other implementation resources on our quality management resources page, including a/an:

Keep the conversation going

If you have ideas about research, guidance or support for the assurance profession or you would like to share what you are seeing in practice, email me directly.

Disclaimer

The views and opinions expressed in this article are those of the author and do not necessarily reflect that of CPA Canada.