New U.S. auditor reporting standard and implications for Canada

The U.S. Public Company Accounting Oversight Board (PCAOB) approved a new auditor reporting standard in June. The standard is subject to approval by the U.S. Securities and Exchange Commission, which may be obtained by October 2017. It contains some significant differences from Canadian auditor reporting standards.

The Auditing and Assurance Standards Board (AASB) is considering these differences in relation to the auditor reporting standards it issued in June 2017, particularly with respect to key audit matter (KAM) reporting.

How the PCAOB standard compares with Canadian standards

The International Auditing and Assurance Standards Board (IAASB) issued a summary comparison between the IAASB and the PCAOB standard. The comparison outlines similarities and differences between the two standards. One of the most important features is that the frameworks for determining audit matter reporting (Key Audit Matters [KAM] under the IAASB standard, and Critical Audit Matters [CAM] under the PCAOB standard) are substantially similar. There are, however, a number of substantive differences. For example:

- the IAASB standard requires more extensive disclosure about the responsibilities of management and the auditor for other information, as well as identification of the other information

- the effective dates are different

- the PCAOB standard requires disclosure of the auditor’s tenure

Effective date of the PCAOB standard

The PCAOB intends that its standard apply to audits as follows:

- provisions other than those dealing with CAM reporting – financial statement fiscal years ending on or after December 15, 2017

- CAM reporting:

- large accelerated filers – financial statement fiscal years ending on or after June 30, 2019

- other filers (other than certain types of issuers that have been specifically exempted) – financial statement fiscal years ending on or after December 15, 2020

KAM reporting for Canada

In Canada, auditor reporting requirements other than KAM reporting are required for audits of financial statements for periods ending on or after December 15, 2018.

The AASB previously planned to initially require KAM reporting for TSX listed entities but decided not to mandate such reporting for any entities in response to Canadian stakeholders. They asked the AASB to wait until the U.S. direction was clear because significantly different audit matter reporting between Canada and the U.S. could create confusion in the marketplace and potentially affect comparability of information across the North American capital markets.

As CAM and KAM reporting are not going to be substantively different, the AASB is now in a position to move forward to decide to which entities KAM reporting should apply and the effective date of those requirements, for example, should KAM reporting apply for TSX listed entities in 2019 or 2020?

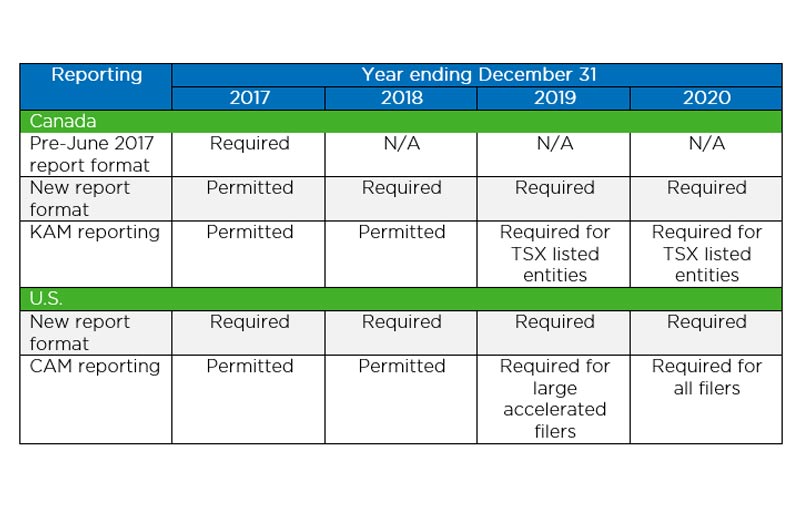

Audits of dual listed entities

With respect to the approximately 280 entities that are listed in both Canada and the U.S., the following table illustrates how auditor reporting may transition:

Under the current reporting regimes, U.S. regulators accept an auditor’s report that complies with both Canadian and PCAOB standards. Well over half of dual listed entity audit reports are presented on this basis. However, with the significant changes to reporting standards on both sides of the border it is uncertain whether regulators will continue to permit such combined reports. The AASB may need to consider whether changes to standards could facilitate continuation of combined auditor’s reports.

Keep the conversation going

The new U.S. reporting standard completes a step change to auditor reporting in North America, in line with developments globally. What are your views on the U.S. developments and the implications for reporting in Canada?

Post a comment below or email me directly.

Conversations about Audit Quality is designed to create an exchange of ideas on global audit quality developments and issues and their impact in Canada.